Omicron Anxiety And What To Watch This Market Week

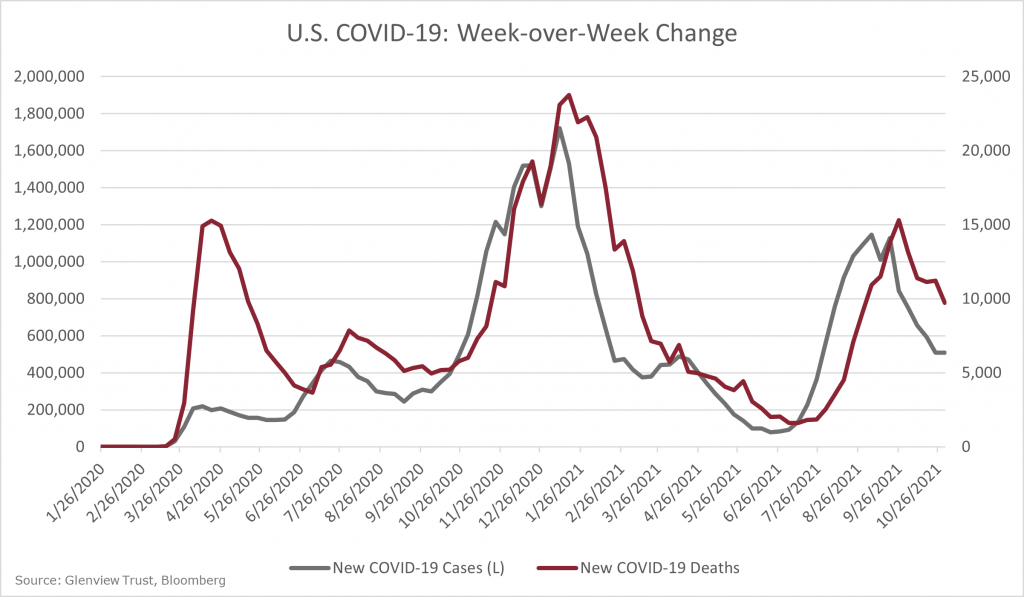

Markets were spooked on Friday by the rise of a new Covid variant, Omicron. Early indications regarding the severity of symptoms and hospitalization rate are encouraging, but much is still unknown. Markets will be watching for any additional information this week.