Why Did Buffett Buy Occidental Petroleum Stock?

Why Did Buffett Buy Occidental Petroleum Stock?

Berkshire now owns an over 14% stake in Occidental Petroleum worth approximately $7.7 billion. This would rank it as one of Buffett’s top ten publicly-traded holdings. Higher oil prices over the long term and the benefits of U.S. production would make this investment a long-term winner.

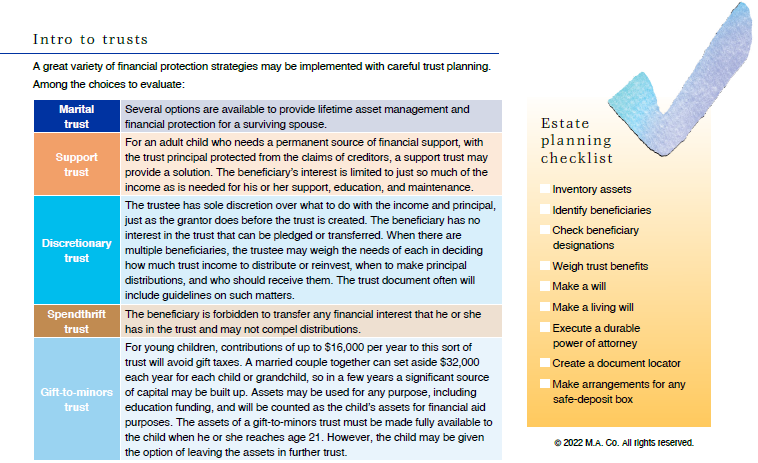

Estate planning without taxes

The Bond Vigilantes Ride Again

The Bond Vigilantes Ride Again

The bond vigilantes have returned to hold the Fed’s feet to the fire to tighten policy in the face of the inflation threat. The yields on short-term bonds reflect aggressive rate hikes. Unless the price shocks derail the job market, odds should still favor higher yields on 10-year Treasury bonds.

What Happens To Stocks And Bonds When The Fed Hikes

What Happens To Stocks And Bonds When The Fed Hikes

Despite last week’s strong rally, stocks have generally traded lower in the three months after a Fed rate increase. Longer-term bonds have usually seen yields increase. The threat of stagflation, recession, and an escalating conflict in Ukraine should keep market volatility elevated.

Inflation Leaves The Fed With No Good Choices

Inflation Leaves The Fed With No Good Choices

The Federal Reserve typically had the option to delay raising rates if the economy faced downside risk or was weakening, but that option is not available due to elevated inflation. Stocks have risen during most tightening cycles but struggle immediately following the first hike.

Is The U.S. Descending Into Recession?

Is The U.S. Descending Into Recession?

While the jobs report and U.S. production provide some solace that the economy can withstand the rising prices, recession odds are increasing. The Fed could be forced to hike rates to curb inflation and break the economy. Interestingly, stocks have typically risen after a recession signal.